Are you an entrepreneur or a small business owner looking for financial assistance to grow your business? Business loans can be a valuable tool to help you achieve your goals. In this comprehensive guide, we will explore everything you need to know about business loans, including their types, benefits, application process, and more. Whether you're a startup or an established company, this article will provide you with valuable insights to make informed decisions regarding business financing.

Introduction

Starting or expanding a business often requires financial resources. Business loans offer entrepreneurs and business owners access to the funds they need to fuel growth, invest in new equipment, hire employees, or consolidate debts. Understanding the different types of business loans, the application process, and the requirements is essential for making informed decisions that align with your business objectives.

Understanding Business Loans

Definition and Purpose

A business loan is a financial product designed to provide capital to businesses for various purposes. It allows business owners to borrow a specific amount of money from a lender, which is then repaid over a predetermined period with interest. Business loans can be used for startup costs, working capital, equipment purchases, expansion projects, and more.

Types of Business Loans

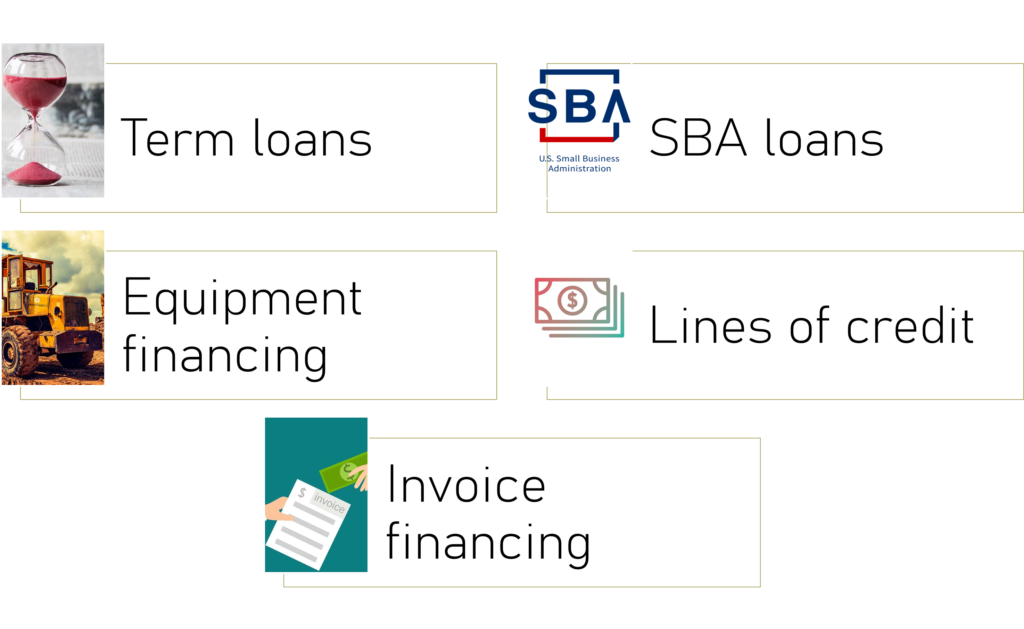

Business loans come in various forms, each tailored to different business needs. Common types of business loans include term loans, SBA loans, equipment financing, lines of credit, and invoice financing. Understanding the characteristics of each loan type can help you determine which option best suits your specific requirements.

Benefits of Business Loans

Business loans offer several advantages to entrepreneurs. They provide immediate access to funds, allowing businesses to seize growth opportunities and address financial challenges promptly. Additionally, business loans can help establish creditworthiness, improve cash flow, and provide tax benefits, making them a valuable resource for business owners.

Eligibility and Requirements

Credit Score and Financial History

Lenders assess the creditworthiness of borrowers before approving a business loan. Maintaining a good credit score and demonstrating a solid financial history increases your chances of obtaining favorable loan terms. Understanding the factors that lenders consider and taking steps to improve your credit profile is crucial.

Business Plan and Documentation

A well-crafted business plan and accurate financial documentation are vital when applying for a business loan. Lenders often require information about your business’s operations, revenue projections, and financial statements. Providing comprehensive and up-to-date documentation showcases your business’s viability and helps lenders evaluate the loan’s risk.

Collateral and Personal Guarantee

Some business loans may require collateral or a personal guarantee to secure the loan. Collateral can include assets such as real estate, equipment, or inventory, providing lenders with a form of security. Personal guarantees, on the other hand, hold the business owner personally responsible for loan repayment if the business defaults.

Finding the Right Lender

Banks and Credit Unions

Traditional banks and credit unions are common sources of business loans. They offer a wide range of loan products, competitive interest rates, and personalized customer service. However, the application process may be more stringent and time-consuming compared to other lending options.

Online Lenders and Alternative Financing Options

In recent years, online lenders and alternative financing platforms have gained popularity. These lenders often provide quicker approval processes, flexible loan terms, and higher approval rates for businesses with less-than-perfect credit. Researching reputable online lenders and considering alternative financing options can broaden your loan possibilities.

Government-Backed Loan Programs

Government-backed loan programs, such as those offered by the Small Business Administration (SBA), provide support to small businesses. These programs offer favorable terms, lower interest rates, and longer repayment periods. Exploring government-backed loan options can be beneficial, particularly for startups and businesses in need of specialized financing.

The Loan Application Process

Research and Preparation

Thoroughly researching loan options, interest rates, and lenders’ requirements is essential before starting the loan application process. This preparation enables you to choose the most suitable loan for your business and gather the necessary documents efficiently.

Gathering Required Documents

Business loan applications typically require various documents, such as financial statements, tax returns, business licenses, and bank statements. Organizing these documents in advance saves time and ensures a smoother application process.

Submitting the Application

Once you’ve gathered all the necessary documents, it’s time to submit your loan application. Follow the lender’s instructions carefully and provide accurate information to avoid delays or potential rejections. Promptly respond to any additional requests from the lender during the review process.

Review and Approval

After submitting your application, the lender will review your information, assess your creditworthiness, and evaluate the risk associated with the loan. This process may involve credit checks, financial analysis, and verification of the provided documentation. Upon approval, you will receive a loan offer outlining the terms and conditions.

Loan Repayment and Terms

Interest Rates and Fees

Interest rates and fees can significantly impact the total cost of borrowing. Understanding the different types of interest rates (fixed or variable) and associated fees (origination fees, prepayment penalties) helps you evaluate the affordability of the loan and plan for repayment accordingly.

Repayment Options

Business loans offer various repayment options, including monthly installments, bi-weekly payments, or flexible repayment schedules. Assessing your business’s cash flow and financial projections can help you choose a repayment plan that aligns with your ability to make timely payments.

Loan Terms and Conditions

Loan terms and conditions outline the specific details of the loan agreement. This includes the loan amount, interest rate, repayment period, collateral requirements, and any additional clauses or restrictions. Thoroughly reviewing and understanding these terms is essential to ensure compliance and avoid any potential issues in the future.

Managing Business Loan Funds

Effective Financial Planning

Proper financial planning is crucial once you secure a business loan. Develop a budget and cash flow forecast to ensure the loan funds are utilized effectively. This includes allocating funds for operational expenses, debt repayment, growth initiatives, and emergency reserves.

Tracking Expenses and Cash Flow

Maintaining accurate financial records and tracking expenses is essential to monitor the loan’s impact on your business’s cash flow. Implementing robust accounting practices and utilizing financial management tools can help you stay on top of your business’s financial health.

Utilizing Funds for Growth

Business loans are often obtained with the goal of fueling growth. Whether it’s expanding operations, investing in marketing strategies, or launching new products/services, strategically utilizing the loan funds to generate a return on investment is vital. Continuously evaluating the effectiveness of your investments ensures optimal use of the loan funds.

Alternatives to Traditional Business Loans

Business Lines of Credit

A business line of credit provides a revolving credit facility, allowing businesses to access funds as needed. It offers flexibility and convenience, giving businesses the ability to address immediate financial needs and manage cash flow fluctuations effectively.

Small Business Grants

Small business grants are non-repayable funds provided by governments, organizations, or foundations to support specific business activities or industries. Researching and applying for relevant grants can provide an alternative source of funding, particularly for businesses with unique characteristics or objectives.

Crowdfunding and Peer-to-Peer Lending

Crowdfunding platforms and peer-to-peer lending networks enable businesses to raise capital from a large number of individuals. These alternative financing options leverage the power of community support and can be a viable solution for startups or businesses with innovative ideas.

Choosing the Right Business Loan

Assessing Your Financial Needs

Before committing to a business loan, carefully evaluate your financial needs. Consider factors such as the loan amount required, repayment capabilities, interest rates, and any specific features or benefits that align with your business objectives.

Comparing Loan Options

Conducting thorough research and comparing multiple loan options allows you to identify the most favorable terms and conditions. Take into account interest rates, fees, repayment flexibility, and customer reviews to make an informed decision.

Consulting with Financial Professionals

If you’re unsure about the best financing option for your business, consider seeking advice from financial professionals such as accountants or business consultants. Their expertise can help you navigate the complexities of business loans and make optimal financial decisions.

Conclusion

In conclusion, business loans are valuable resources that provide entrepreneurs and business owners with the capital needed to grow and expand their ventures. By understanding the different types of business loans, the application process, and the requirements, you can make informed decisions and secure financing that aligns with your business goals. Remember to evaluate your financial needs, research lenders, and manage loan funds effectively to maximize the benefits of business loans.

FAQs (Frequently Asked Questions)

What is the minimum credit score required to qualify for a business loan?

The minimum credit score required to qualify for a business loan varies depending on the lender and the type of loan. Generally, a credit score above 600 is considered favorable, but some lenders may have stricter requirements.

Can I get a business loan with bad credit?

While having bad credit can make it more challenging to qualify for a business loan, there are lenders who specialize in providing loans to businesses with less-than-perfect credit. These lenders may have different eligibility criteria and may offer loans at higher interest rates.

How long does it take to get approved for a business loan?

The time it takes to get approved for a business loan can vary. It depends on factors such as the lender’s review process, the complexity of the loan application, and the completeness of the documentation provided. Some online lenders offer quicker approval times compared to traditional banks.

What is the difference between a secured and an unsecured business loan?

A secured business loan requires collateral, such as assets or property, to secure the loan. In case of default, the lender can seize the collateral to recover their funds. In contrast, an unsecured business loan does not require collateral but may have higher interest rates to compensate for the increased risk.

Can I use a business loan to start a new business?

Yes, business loans can be used to start a new business. However, lenders may require a solid business plan and financial projections to assess the viability of the business. Startups may also explore alternative financing options such as small business grants or crowdfunding.